- While not explicitly mandated by regulation, adverse media screening is considered a regulatory expectation for risk-based AML programs, especially for higher-risk customers.

- At a minimum, screen adverse information against OFAC sanctions, UN sanctions, PEP lists, and regulatory enforcement databases. Consider adding adverse media, criminal databases, and country-specific watchlists based on your risk profile.

- Keep all screening records, investigation documentation, and risk decisions for at least five years. Some jurisdictions may require longer retention periods for certain types of records.

My manager asked me to write something about adverse information after one of our leads described their compliance issues last month. Honestly, I wasn’t sure where to start – there’s so much stuff out there, and half of it contradicts the other half.

Been working in fintech for a while now and adverse information is one of those things that sounds simple but gets complicated fast. You’re screening names, checking databases, trying to figure out if John Smith in London is the same John Smith who’s on some watchlist. Fun times.

Anyway, figured I’d put together what I’ve learned from talking to compliance teams, reading through way too many whitepapers, and trying to make sense of what actually matters versus what’s just regulatory theater.

Before anything, here are some nuts and bolts.

Adverse Information is Negative Data Used in AML Risk Assessment

Basically, adverse information is all the bad stuff that shows up when you’re checking someone out. Think criminal records, being on a sanctions list, getting busted for fraud – anything that makes you go, ‘hmm, that’s not good.’

Main types you’ll run into:

- Sanctions lists – Government lists of people/companies you can’t do business with

- Criminal stuff – Arrests, convictions, ongoing investigations for financial crimes

- Bad press – News articles about corruption, fraud, sketchy business dealings

- Regulatory actions – When regulators fine someone or take enforcement action

- Politicians and their families – PEPs who might be involved in corruption

- Court problems – Bankruptcies, lawsuits, other legal mess that show financial issues

The whole point is you’re trying to figure out if this person or company is sketchy before you do business with them. AML rules and Customer Due Diligence requirements basically say you have to check for this stuff – it’s not optional. Miss something obvious, and regulators will not be happy with you.

Adverse Information Monitoring Must Be Ongoing in Nature

You can’t just check someone once and call it done – adverse information monitoring has to be ongoing. People’s situations change, and new stuff comes up constantly.

Think about it – someone might be clean when they open an account, but six months later, they get arrested for fraud. Or they weren’t on any sanctions list initially but then got added after some investigation. Maybe they just got elected to a government position and became a PEP.

The watchlists get updated all the time too. New sanctions, criminal cases, negative news. If you’re only checking at account opening, you’re missing everything that happens after. Most places run automated scans monthly or quarterly, plus set up alerts for major changes. Because finding out your customer has been sanctioned for three months without knowing is not a good look.

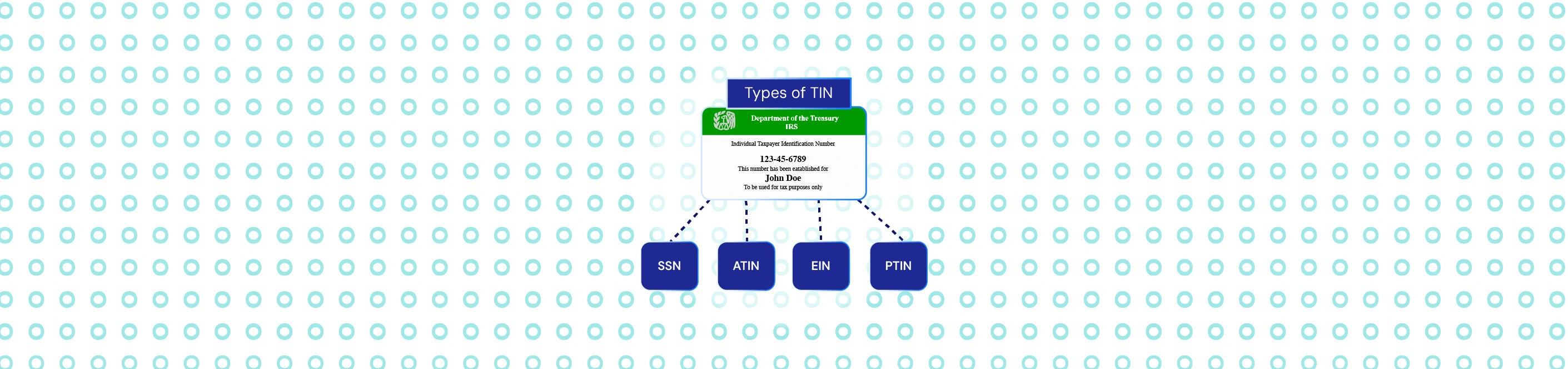

Adverse Information Requirements in AML Regulations

Adverse information only helps if your systems are built to detect and act on it. Regulators expect clear processes that align with U.S. AML laws under the Bank Secrecy Act, enforced by FinCEN and guided by FATF standards.

Customer Due Diligence (CDD)

The CDD rule requires risk-based screening during onboarding but doesn’t tell you exactly what to screen against. Here’s what most places actually do:

- Sanctions screening – OFAC, UN, EU lists at minimum. Some add country-specific lists depending on your customer base

- PEP databases – World-Check, Dow Jones, or similar commercial sources for politically exposed persons and their families

- Negative media screening – Automated searches for criminal activity, fraud allegations, regulatory actions

- Criminal background checks – For higher-risk customers, though this varies by institution and jurisdiction

- Regulatory enforcement databases – SEC actions, banking violations, insurance commissioner enforcement

The key is documenting your risk-based approach – why you screen certain customers more thoroughly than others. High-net-worth clients, foreign nationals, and people in certain industries all get more scrutiny.

Enhanced Due Diligence (EDD)

When adverse information screening turns up hits, you’re automatically in EDD territory.

PEPs, anyone with a criminal history, negative media coverage about fraud or corruption – they all trigger enhanced procedures. This means additional documentation, senior management approval, more frequent monitoring, and often restrictions on certain products or services.

The key is having clear policies about what constitutes a “hit” versus a false positive.

Record-Keeping and Reporting

Document your entire process – what sources you searched, what you found, how you evaluated the results, and your final risk decision. If adverse information suggests potential money laundering or sanctions violations, you need to file a SAR within 30 days.

Keep everything for five years minimum. Examiners love to trace through your adverse information cases to see if your controls actually work.

Adverse Information vs. Adverse Media: Key Differences

Basically, adverse information is the umbrella term for all the bad stuff you need to check for. Adverse media is just one piece of that puzzle – specifically the news and media coverage part.

| What It Is | Adverse Information | Adverse Media |

| The Big Picture | Everything negative – sanctions, criminal records, court cases, regulatory actions, bad press | Just the news/media part – articles, press releases, investigative reports |

| Where It Comes From | Government lists, court databases, regulatory sites, OFAC, news outlets | News websites, newspapers, blogs, social media, press releases |

| How Reliable | Usually, official/verified sources | Can be allegations or rumors – needs fact-checking |

| How Often Updated | Depends – OFAC updates daily, court records weekly/monthly | Constantly – news breaks 24/7 |

| How You Screen | Database searches, list matching | Keyword searches, AI text analysis |

| Example | John Smith on OFAC sanctions list | News article: “John Smith investigated for fraud” |

The key thing is you need both.

Official databases catch the formal stuff, but adverse media often picks up investigations or allegations before they hit the official lists. Just remember that media reports aren’t always facts – someone being “linked to” something in a news article isn’t the same as being convicted.

How to Conduct Adverse Information Screening at Scale (Without Drowning Your Team)

So you’re trying to screen thousands of customers, and your team is basically dying. Everyone named John Smith triggers like 50 alerts, most of which are obviously not the right person.

The problem gets worse when you scale up. What worked when you had 20 new customers a week doesn’t work when you have 200 a day. Manual searches take forever; different people get different results for the same person and don’t even get me started on trying to rescreen your entire customer base every month.

APIs basically solve this by doing the boring stuff automatically.

Good ones will pre-filter the garbage matches and only show you results that might actually be relevant. Instead of manually searching five different databases, you hit one endpoint and get everything back ranked by how likely it is to be a real match.

That’s why we built our adverse screening APIs to handle global sanctions, PEP databases, and media monitoring through simple integrations. Want to see how much time your team could save? Book a demo with us.

FAQs

What is adverse information on a credit report?

Adverse information on a credit report refers to a history of missed or late payments on loans or credit cards.

How do I remove adverse information from a credit report?

You can dispute incorrect or outdated negative information by contacting the credit bureau through their website or call center. If the entry is wrong, the bureau may remove it after review.

What is adverse media screening in KYC?

Adverse media screening is part of AML and KYC processes. It involves checking media sources for negative news about individuals or businesses you are working with.

Do we need to screen every customer or just high-risk ones?

You need basic sanctions screening for everyone, but the depth of adverse information screening can be risk-based. Higher-risk customers require more comprehensive screening across multiple databases